2026 Bonus Tax Calculator: Percentage vs. Aggregate Method

Quick Answer: 2026 Bonus Tax Calculator: Percentage vs. Aggregate Method — Uses 2026 IRS Publication 15-T brackets, current FICA rates (Social Security 6.2% up to $184,500; Medicare 1.45%), and state-specific withholding tables. All calculations run in your browser. No data is stored. Reviewed by our payroll compliance team.

Why does your bonus get withheld at 22% when your salary is only taxed at 12%? Calculate exactly how much of your 2026 bonus you'll keep after taxes — and how to reduce the hit.

📊 Both withholding methods✓ 2026 IRS Confirmed💰 401(k) strategy included🔒 No data stored

Advertisement

🧮 2026 Bonus Tax Calculator

Required for Aggregate method calculation

Social Security stops at $184,500

Your Bonus Take-Home Pay

$0.00

Description

Amount

💵 Gross Bonus

—

🏛 Federal Tax Withheld

—

🔒 Social Security (6.2%)

—

🏥 Medicare (1.45%)

—

🗺 State Income Tax

—

Total Withheld

—

✅ Net Bonus Take-Home

—

⚠️ Withholding estimate only. Actual tax owed is reconciled on your annual return — if over-withheld you receive a refund, if under-withheld you owe the difference. Consult a tax professional for exact planning.

Why Bonuses Are Taxed at 22% (And How to Reduce It)

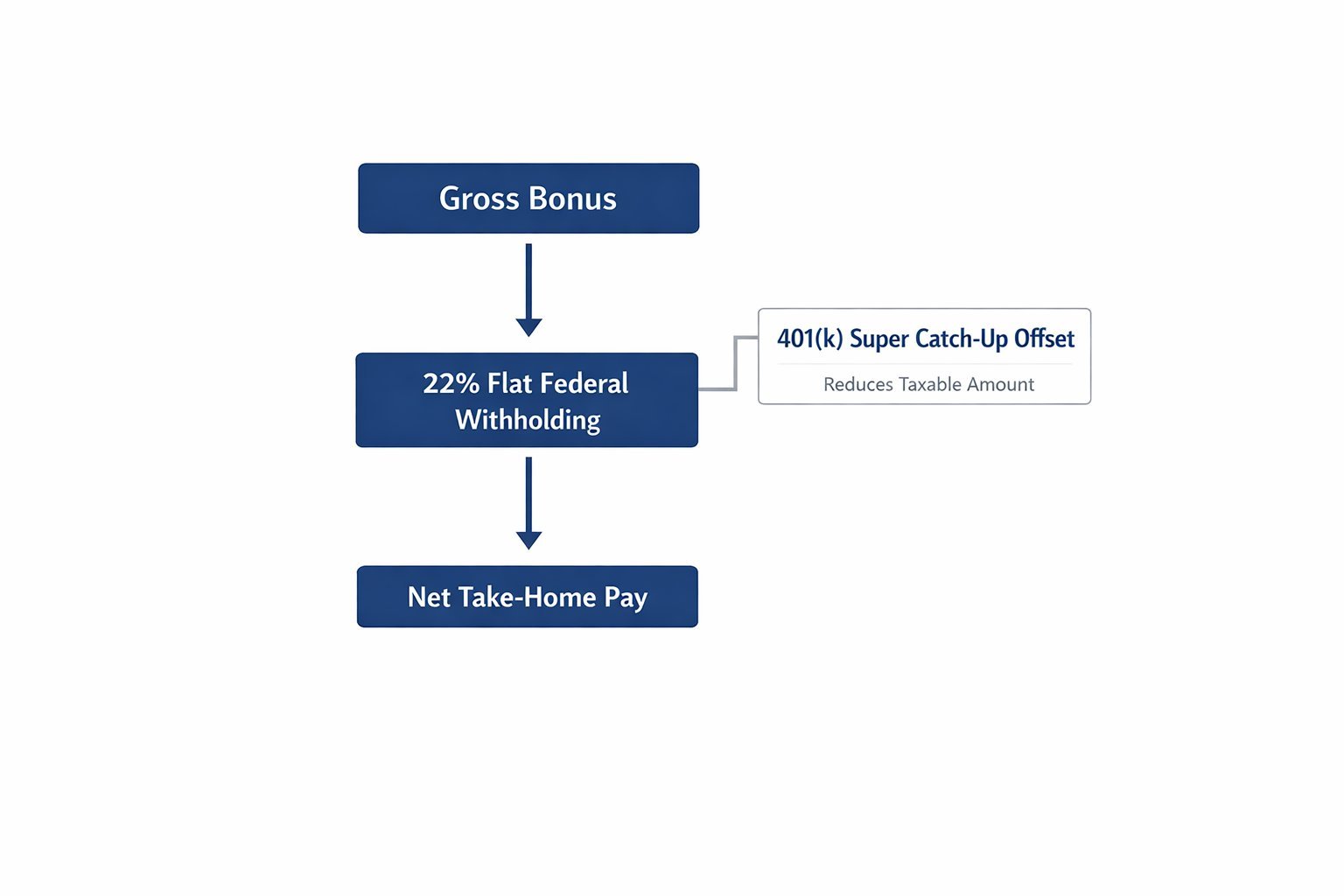

The IRS treats bonuses as "supplemental wages" — separate from your regular wages. When paid as a standalone check, federal law requires employers to use the 22% flat withholding rate for amounts up to $1 million. This often surprises workers who are in the 10% or 12% bracket for their regular income.

The good news: the 22% is just withholding, not your actual tax rate. When you file your 2026 return, your total income is calculated holistically — if your effective rate is lower than 22%, you'll get the difference back as a refund.

💡 Every dollar contributed to a pre-tax 401(k) reduces your federal taxable income. If you're expecting a bonus, ask your HR department to temporarily increase your 401(k) withholding rate for the bonus check — this can significantly reduce the tax hit at the source.

Percentage vs. Aggregate Method: Which Is Better?

For most workers in the 10-22% bracket, the Percentage Method (22% flat) often results in over-withholding — meaning you'll get money back at tax time. For workers in the 32-37% bracket, the Aggregate Method may actually result in less withholding than their true rate. Use the calculator above to compare both methods for your situation.

The IRS classifies bonuses as 'supplemental wages.' When paid separately from your regular paycheck, employers must withhold federal income tax using the flat 22% supplemental wage rate — regardless of your actual tax bracket. This is called the Percentage Method. If your bonus is added to your regular pay in the same check, employers use the Aggregate Method, which may result in higher withholding.

The Percentage Method applies a flat 22% federal withholding on bonus amounts up to $1 million. It's simpler and often results in lower withholding for high earners. The Aggregate Method combines your bonus with regular wages and withholds based on your total income bracket — this can push you into a higher bracket temporarily and result in more withholding, though you'll reconcile the difference at tax time.

The most effective strategies: (1) Maximize your 401(k) contribution — the OBBB raised the 2026 limit to $23,500, with a Super Catch-Up of $35,750 for ages 60-63. Pre-tax 401(k) contributions directly reduce your taxable income. (2) Contribute to an HSA if eligible. (3) Ask your employer about timing the bonus across tax years. (4) Make sure any overtime deduction (up to $12,500) is applied on your return.

Yes. Social Security (6.2%) and Medicare (1.45%) apply to all bonus income just like regular wages. The Social Security portion stops once your total wages exceed $184,500 for 2026. If you've already earned more than $184,500 in regular wages before receiving your bonus, no Social Security tax applies to the bonus.

Under SECURE 2.0 and confirmed for 2026, workers aged 60-63 can contribute up to $35,750 to their 401(k) — that's the standard $23,500 limit plus an enhanced catch-up of $11,250 plus the standard catch-up ($1,000). This is significantly higher than the regular catch-up available to workers 50-59 ($30,500 total). Contributing more to your 401(k) directly reduces your taxable income and can lower the effective rate on your bonus.

For bonus amounts exceeding $1 million in a calendar year, the IRS requires employers to withhold at the highest marginal rate of 37% on the amount over $1 million. The first $1 million is withheld at 22%. This is an automatic mandatory withholding rate — not optional. High earners who receive large bonuses should plan for this withholding and consult a tax professional.

The OBBB does not directly change bonus withholding rates. However, it increases the standard deduction to $16,100 (single), which reduces your overall taxable income for the year and may lower your effective tax rate. Additionally, if you work overtime, the No Tax on Overtime deduction (up to $12,500) can reduce your total federal income tax liability when you file, partially offsetting bonus taxes.

For a separately-paid bonus: multiply the gross bonus by 0.78 (100% minus 22% federal withholding) then subtract Social Security (6.2%) and Medicare (1.45%) if applicable, and any state income tax. Example: $10,000 bonus → $7,800 after 22% federal → subtract FICA ($765) → subtract state tax → approximately $7,000 net for a no-state-tax state. Use the calculator above for your specific scenario.