2026 Federal Income Tax Calculator

Advertisement

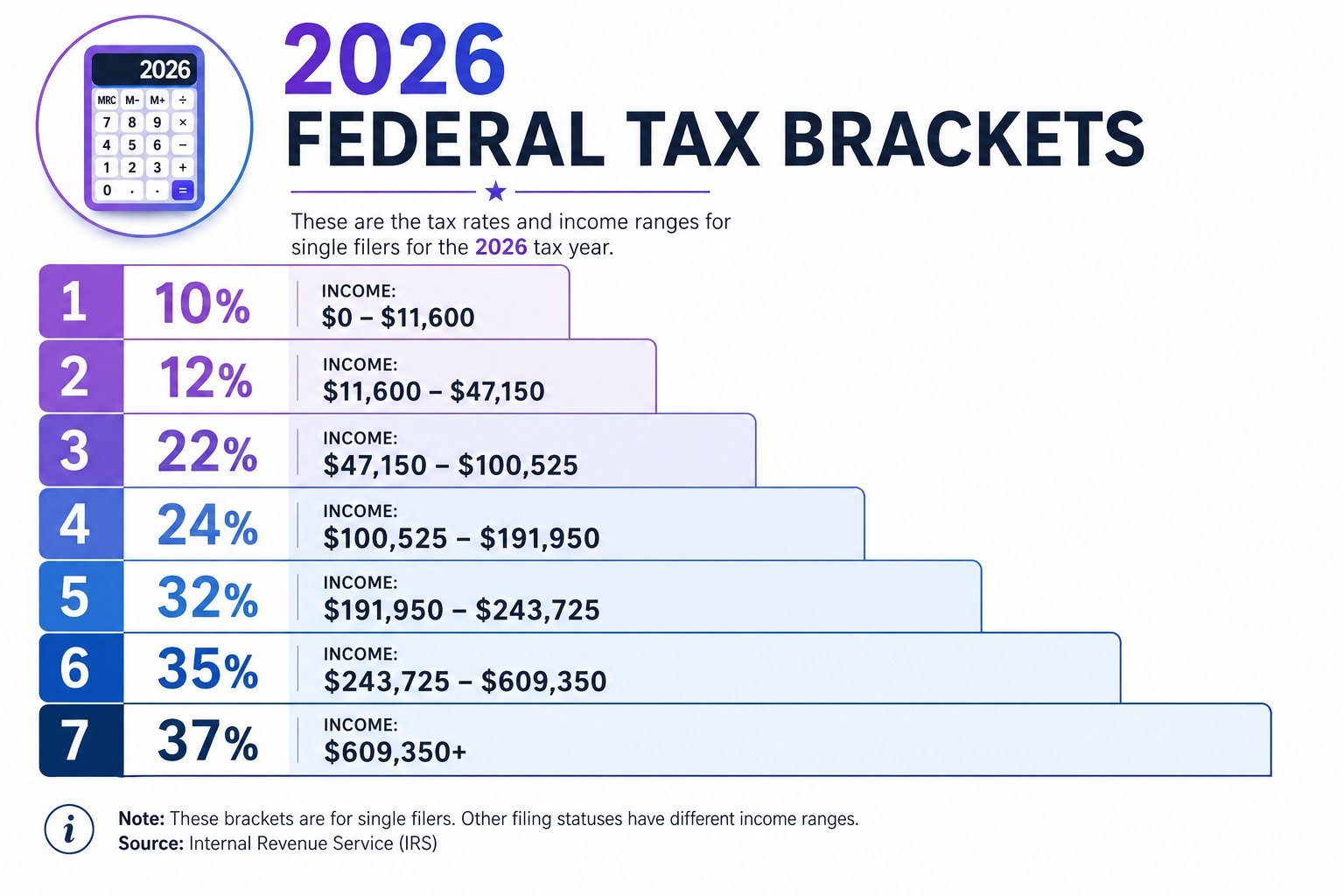

What are the 2026 federal tax brackets?

For 2026, federal tax brackets for single filers are: 10% ($0-$11,600), 12% ($11,601-$47,150), 22% ($47,151-$100,525), 24% ($100,526-$191,950), 32% ($191,951-$243,725), 35% ($243,726-$609,350), and 37% (over $609,350). These are marginal rates applied progressively to different portions of your taxable income.

2026 federal tax brackets with inflation-adjusted income thresholds for single filers

2026 Federal Income Tax Brackets

The IRS adjusts federal tax brackets annually for inflation. For 2026, the standard deduction is $14,600 for single filers, $29,200 for married filing jointly, and $21,900 for head of household. Understanding these brackets helps you calculate your tax liability accurately and plan for the year ahead.

Single Filers Tax Brackets 2026

| Tax Rate | Income Range | Tax Owed |

|---|---|---|

| 10% | $0 to $11,600 | 10% of taxable income |

| 12% | $11,601 to $47,150 | $1,160 + 12% of amount over $11,600 |

| 22% | $47,151 to $100,525 | $5,426 + 22% of amount over $47,150 |

| 24% | $100,526 to $191,950 | $17,168.50 + 24% of amount over $100,525 |

| 32% | $191,951 to $243,725 | $39,110.50 + 32% of amount over $191,950 |

| 35% | $243,726 to $609,350 | $55,678.50 + 35% of amount over $243,725 |

| 37% | Over $609,350 | $183,647.25 + 37% of amount over $609,350 |

How Federal Income Tax Works

Federal income tax uses a progressive system where your income is divided into brackets, each taxed at a different rate. You don't pay your highest rate on all your income—only on the portion that falls within each bracket. For example, if you're single and earn $60,000 in 2026, you first subtract the standard deduction ($14,600), leaving $45,400 in taxable income. The first $11,600 is taxed at 10%, and the remaining $33,800 is taxed at 12%. This progressive structure means your effective tax rate (the average rate you actually pay) is always lower than your marginal rate (your highest bracket).

Understanding the difference between marginal and effective tax rates is crucial for tax planning. Your marginal rate is what you'll pay on your next dollar of income, while your effective rate represents your overall tax burden. At $60,000 of gross income ($45,400 taxable), your marginal rate is 12%, but your effective rate on taxable income is only about 10.5%. When people say they're "in the 22% tax bracket," they're referring to their marginal rate, not what they pay on their entire income.

Standard Deduction vs. Itemizing

The standard deduction for 2026 is $14,600 for single filers, $29,200 for married filing jointly, and $21,900 for head of household. This amount is subtracted from your gross income before calculating your taxable income. Most taxpayers (about 90%) use the standard deduction because it's larger than their itemized deductions. Itemizing makes sense if your deductible expenses—including mortgage interest, property taxes (capped at $10,000 by SALT limitations), charitable contributions, and medical expenses exceeding 7.5% of your AGI—exceed your standard deduction amount.

Frequently Asked Questions

How do I calculate my federal tax?

To calculate federal tax: (1) Start with your gross income, (2) Subtract the standard deduction ($14,600 for single filers in 2026) or itemized deductions, (3) Apply the appropriate tax rate to each bracket of your taxable income, and (4) Sum the tax from all brackets. The calculator above does this automatically.

What is the standard deduction for 2026?

The 2026 standard deduction is $14,600 for single filers and married filing separately, $29,200 for married filing jointly and qualifying widow(er)s, and $21,900 for head of household. This is an increase from 2025 due to inflation adjustments.

What is my effective tax rate vs marginal rate?

Your marginal tax rate is the percentage you pay on your last dollar of income—your highest bracket. Your effective tax rate is the average rate you pay on all your income. For example, at $60,000 gross ($45,400 taxable for single filers), your marginal rate is 12% but your effective rate on taxable income is about 10.5%.

Are federal tax brackets based on gross or taxable income?

Federal tax brackets are applied to your taxable income, not gross income. Taxable income is your gross income minus the standard deduction (or itemized deductions) and any other above-the-line deductions. This is why someone earning $60,000 gross doesn't pay tax on the full $60,000.

How much federal tax will I owe on $50,000?

On $50,000 gross income as a single filer in 2026, you'll have $35,400 taxable income after the $14,600 standard deduction. Your federal tax will be approximately $4,106: $1,160 on the first $11,600 (10%) plus $2,946 on the remaining $23,800 (12%).

How much federal tax on $100,000 salary?

On $100,000 gross as a single filer, after the $14,600 standard deduction, you'll have $85,400 taxable income. Your federal tax will be approximately $14,908: $1,160 (10% bracket) + $4,266 (12% bracket) + $8,482 (22% bracket). Your effective rate is about 14.9%.

When are federal taxes due in 2026?

Federal income taxes for tax year 2025 are due on April 15, 2026. For tax year 2026 (the income you earn this year), taxes will be due April 15, 2027. If you're self-employed or have substantial income not subject to withholding, you may need to make quarterly estimated payments.

How are capital gains taxed in 2026?

Long-term capital gains (assets held over 1 year) are taxed at 0%, 15%, or 20% depending on your income, separate from ordinary income brackets. Short-term capital gains (assets held 1 year or less) are taxed as ordinary income at your marginal tax rate.

What income is exempt from federal tax?

For 2026, income up to the standard deduction amount is effectively exempt: $14,600 for single filers, $29,200 for married filing jointly. Additionally, certain types of income are completely exempt, including qualified Roth IRA distributions, most municipal bond interest, and gifts/inheritances received.

Can I reduce my federal tax liability?

Yes, several strategies can reduce federal tax: maximize pre-tax retirement contributions (401k, Traditional IRA), take advantage of tax credits (Child Tax Credit, Earned Income Credit), use HSA contributions, harvest capital losses to offset gains, and bunch deductions to exceed the standard deduction in alternating years.

How does married filing jointly affect federal tax?

Married filing jointly doubles most tax brackets and the standard deduction ($29,200 in 2026), often resulting in lower combined tax for couples. However, if both spouses have similar high incomes, they may experience a "marriage penalty" where their combined tax exceeds what they'd pay filing as two single people.